When Nigeria introduced point-of-sale (PoS)–based agency banking in 2013, the policy goals include reduction of reliance on cash, deepen financial inclusion by extending basic financial services to communities underserved by traditional banks. More than a decade later, that payment-layer innovation has evolved into something larger, a digital public infrastructure that is reshaping livelihoods, creating jobs, and transforming rural economies. Reports Muhammad Auwal Ibrahim.

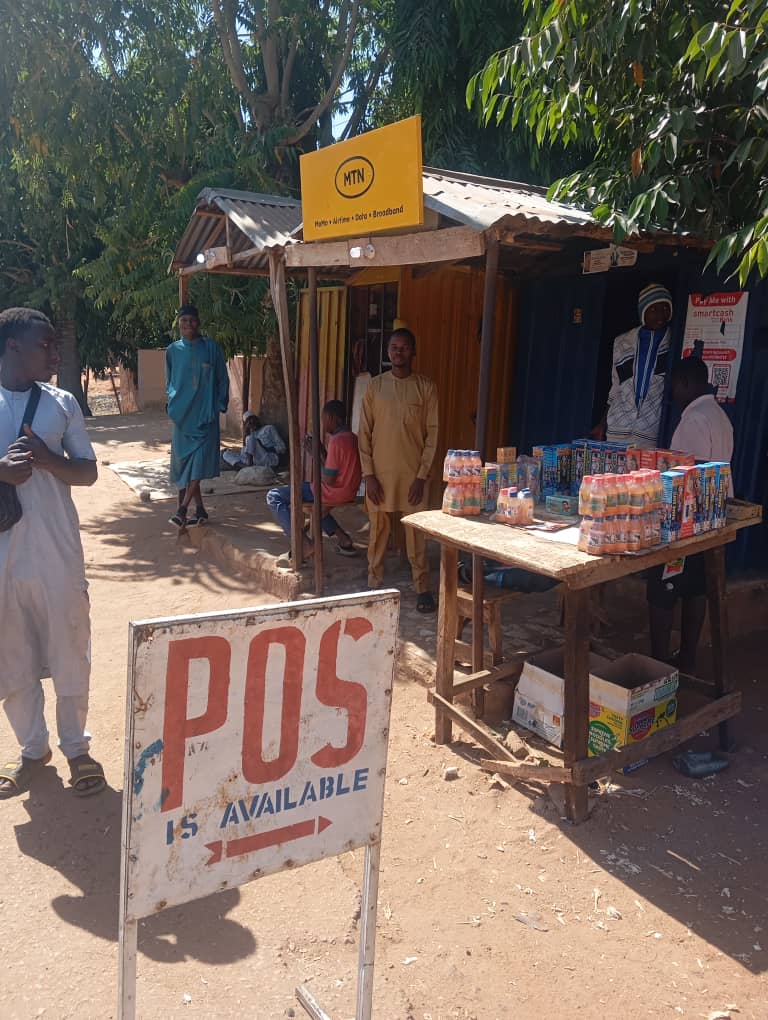

On most mornings in Kwami Gari, a rural community in Kwami local government area of Gombe state, Muhammad Sagir Abubakar sits before a small aluminium kiosk tapping at a point-of-sale terminal powered by a mobile network.

Customers arrive steadily, withdrawing small sums like ₦500, ₦2,000, or ₦5,000, transactions that once required long, costly trips to Gombe town, the nearest city with banking facilities.

A decade ago, Abubakar would have had to travel about 30 kilometres to Gombe town to access a bank or an ATM. The trip often consumed a large portion of whatever money he hoped to withdraw. With no stable job, he depended on seasonal farm work to survive.

“Before, I couldn’t get money unless I worked on the farm,” he said. “Now, with PoS, I am earning a living and even helping others.”

Muhammad Sagir Abubakar, a PoS agent in Kwami LGA.

Today, Abubakar is one of the numerous informal financial agents operating within Nigeria’s instant payment ecosystem, a shared, interoperable digital payment layer that connects banks, fintechs, telecoms and end users, even in places without physical bank branches.

From financial inclusion to employment opportunities

Nigeria launched point-of-sale-based agency banking in 2013 as part of a broader push for digital financial inclusion. The idea was simple: allow individuals and small businesses to act as banking agents, offering cash withdrawals, transfers and bill payments through fintech platforms.

What policymakers may not have fully anticipated was how deeply the system would reshape livelihoods, particularly among unemployed and underemployed youth.

In Kwami local government area of Gombe State, there is still no traditional bank branch. Yet residents now access basic financial services within walking distance, thanks to fintechs companies that have transformed roadside stalls and market corners into banking points.

As traditional banks remained concentrated in cities, fintech companies filled the gap, leveraging Nigeria’s digital payment infrastructure to deliver services at scale.

Abubakar joined the PoS business at 25, after years of scraping by through farm labour and tailoring jobs. Five years later, he says the income has allowed him to buy land and begin building a house, an achievement that once felt unimaginable.

“Many young people are into PoS now,” he told Daily Episode. “It has changed our lives.”

Bridging gaps left by traditional banking

Despite Nigeria’s financial inclusion drive, more than 28.8 million adults remain unbanked, according to Enhancing Financial Innovation and Access (EFInA). Rural communities account for a disproportionate share, held back by poor infrastructure, poverty and the absence of bank branches.

Nigeria’s financial inclusion stands at about 74 per cent nationally, but the figure masks sharp regional disparities.

Across Nigeria, stories like Abubakar’s are becoming common as fintech-enabled payment systems absorb some of the country’s unemployed population.

For residents of Kwami, the impact is tangible.

“We suffered before PoS,” said Aliyu Muhammad, 28, who operates multiple terminals in Unguwan Sarki, another community in the area. “We had to travel to Gombe just to withdraw ₦2,000 or ₦5,000 and queue for hours.”

Aliyu Muhammad, another PoS agent in Kwami

Today, people withdraw as little as ₦500 within their communities. Muhammad employs three operators across three machines, creating jobs in a place where opportunities are scarce.

“PoS helps me sustain my family,” he said. “I have employed other people to work with me, boosting the local economy.”

Economic ripple effects

The expansion of instant digital payments has reshaped local commerce, not just access to cash.

Abubakar Usman, a trader in Shongo Sarkin Yaki village, Kwami LGA, said access to digital payments has expanded financial participation, which has reshaped commerce.

He said, “Financial inclusion has increased,” because more people in his village now have bank accounts

With interoperable digital payment options, traders like him no longer turn away customers who lack cash. Buying and selling have increased, and money circulates faster within the community.

“It has reduced the stress of travelling long distances just to access cash,” Usman said.

Youth, skills and digital economy

Beyond direct PoS operations, Nigeria’s payment-layer DPI has opened pathways into the broader digital economy for younger Nigerians.

Fintechs’ Business Relationship Managers (BRMs) earn commissions on PoS transactions for every customer they sell machines to, creating thousands of income streams.

Hussaini Suleiman was a third-year engineering student at Abubakar Tafawa Balewa University when he began working with Moniepoint in Gombe. He describes the role as a blend of sales, customer service and technology.

Hussaini Suleiman, a business relationship manager at Moniepoint

“You don’t need a degree to start,” he said. “But you need communication skills.”

Through fintech, Suleiman started a business and expanded into telecommunications services. He said customers trust digital platforms for their speed and reliability, especially compared with cash transactions.

“Communication and social skills help you win customers,” he said. “For Moniepoint, most of our skills are taught in a course, which is mandatory for every worker. We are also doing quarterly exams for the course you have studied.”

Constraints within the system

The system is not without problems. Agents face fraud, fake transfer alerts, network failures and limited operating capital.

“Low capital is a major challenge,” Muhammad said. “Someone may ask you to transfer ₦2 million, but you don’t have it in your wallet.”

He further cited unpaid debts from customers and unreliable mobile networks that can halt transactions for hours.

Like Muhammad, Usman faces the challenge of low capital.

“Dealing with different customer behaviours is another challenge we face.”

Still, many agents say the benefits outweigh the risks.

“I can’t take any job paying less than ₦100,000 a month now,” Abubakar said, laughing. “PoS has changed my life entirely.”

Beyond banking: a public digital foundation

Adam Muhammad Ibbi, a financial analyst based in Damaturu, said fintech is creating significant job opportunities, particularly at the grassroots level.

According to him, fintech firms recruit more people than traditional banks, whose hiring processes are often lengthy and restrictive.

“For me, fintech is the future. It makes transactions easier regardless of geographical location and provides employment for thousands of people across the country,” Ibbi said.

He added that financial inclusion drives economic growth by expanding access to financial services to all segments of society.

This report is produced under the DPI Africa Journalism Fellowship Programme of the Media Foundation for West Africa and Co-Develop.