When Isma’eel Muhammad Yahaya made an inter-bank transfer in Kano, he did not expect to wait more than a month for his money to return. The transaction failed, and what followed were weeks of visits to bank branches, repeated follow-ups, and unanswered complaints.

“They said I had to wait for the other bank to respond,” he recalled.

“I only got information when I kept following up.”

The experience, he said, has left him anxious about using digital payment channels.

His experience mirrors a pattern previously published by WikkiTimes, where POS agents across Kano described being forced to advance cash to customers while waiting endlessly for failed or disputed transfers to be reversed. Others reported losing money entirely after falling victim to fraudulent transfers and social engineering scams, with little support from banks or payment service providers.

“Now I’m scared every time I want to make a transfer.”

Stories like Isma’eel’s are not unheard of across Nigeria’s fast-growing digital payments ecosystem, where instant transfers now power everyday commerce but dispute resolution often moves painfully slowly.

A policy response to a systematic problem

Now, the Central Bank of Nigeria (CBN) says it wants to change that.

On January 21, 2026, in Lagos, the Central Bank of Nigeria (CBN) disclosed that banks and other financial institutions have agreed to reduce their response time to electronic fraud incidents to under 30 minutes as part of renewed efforts to curb rising losses in the digital payments ecosystem.

The disclosure was made by the CBN Deputy Governor for Financial System Stability, Philip Ikeazor, at the 2026 Nigeria Electronic Fraud Forum (NeFF) Technical Kick-Off Session.

“The industry has agreed to reduce fraud response times to under 30 minutes, a decisive step that materially improves recovery outcomes and limits systemic exposure,” Ikeazor said, noting that delays in responding to fraud incidents often worsen losses and weaken public confidence in electronic payment channels.

He added that Nigeria is also migrating to the ISO 20022 messaging standard to improve traceability, analytics, and early fraud detection across payment systems.

Digital payments, DPI and the cost of delay

Digital payments are now deeply embedded in Nigeria’s daily life, from salaries and school fees to market purchases and transport fares. This expansion rests on Nigeria’s Digital Public Infrastructure (DPI): the shared rails that connect banks, fintechs, payment switches, identity systems, and data-sharing frameworks.

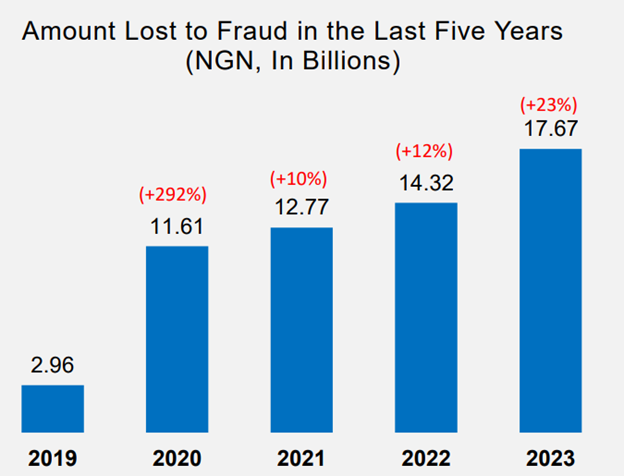

As digital transaction volumes have grown, incidents of fraud and complaints about failed transfers and delayed reversals have attracted greater regulatory attention, even though recent NIBSS data shows fraud losses declined in 2025 after a spike in 2024.

Previous WikkiTimes investigations found that many POS agents and customers routinely absorb losses when transactions go wrong, while weak dispute resolution processes leave victims stranded for days or weeks. Agents reported that banks often shift responsibility between sending and receiving institutions, with customers caught in the middle.

In a DPI-driven system, instant payments depend on real-time communication between multiple institutions. When something goes wrong, that same infrastructure must enable rapid data exchange, transaction tracing, and coordinated action. Where these links are weak, delays become inevitable and costly.

For POS operators, the consequences of slow reversals can be devastating.

“When a transfer fails, the customer expects cash immediately,” said Ibrahim Usman, a Kano-based businessman who also operates a POS outlet.

“If I refuse, there will be an argument. If I pay from my pocket, I may not recover the money. So this 30-minute rule is good news, but we will judge it by how fast they actually return money, not by announcements.”

The CBN’s new timeline appears intended to close this gap by forcing institutions to act quickly once a fraud report is lodged, potentially enabling faster freezing, tracing, and recovery of funds across the payments infrastructure.

Speed Meets Infrastructure

At its core, the directive speaks to Nigeria’s DPI, the interconnected systems that support payments, identity verification, and data exchange across banks and fintech platforms.

Instant transfers depend on seamless communication between multiple institutions. When a dispute arises, those same systems must exchange information quickly and accurately for reversals or blocks to occur. But structural weaknesses persist.

An earlier WikkiTimes report showed that many complaints stall because communication between institutions is slow, and customers are rarely given clear information about the status of their cases.

Yet analysts warn that speed alone will not fix deeper structural issues within Nigeria’s digital payments DPI.

Ahmed Idris, founder of Enovate Lab and a technology and innovation strategist with a strong focus on fintech, digital products, and emerging technologies in Nigeria, believes the directive will help improve user confidence, especially among everyday users who are often the most affected and least protected when such incidents happen.

He said, “A 30-minute response window forces banks and payment institutions to take fraud reports more seriously and treat them as urgent, which is a big step forward for consumer protection.”

However, he cautioned that safeguards are also needed to prevent abuse.

He said, “Those who could deliberately initiate transactions, receive value, and then falsely report fraud. Without proper verification and investigation processes, the policy could create room for abuse and unnecessary disputes.”

Idris also pointed to capacity and coordination gaps within the system.

“There’s also the issue of inter-bank coordination. Many fraud cases involve multiple institutions, and delays can happen when responsibility is unclear or data sharing is slow.”

He warned that response timelines should not become a box-ticking exercise. “If institutions simply acknowledge complaints within 30 minutes without real action, the directive may lose its impact. For it to truly work, banks and fintechs need stronger internal processes, better fraud detection systems, real-time monitoring, and clearer escalation frameworks.”

Generally, he said fintechs and banks need to tighten security and be more intentional in how they design financial products, especially around user education, transaction confirmation, and dispute resolution, stressing that while the directive is a good move, its success will depend more on execution than policy alone.

Standards, Supervision and Trust

At the Nigeria Electronic Fraud Forum where the Central Bank of Nigeria’s 30‑Minute Response requirement was announced, Premier Oiwoh, CEO of the Nigeria Inter‑Bank Settlement System (NIBSS), stressed that reducing fraud losses and improving response times is central to deepening financial inclusion and trust in digital payments.

In her presentation, the CBN Director, Payment System Supervision and NeFF Chairman, Dr. Rakiya Yusuf, said the apex bank would soon begin inspections of banks to ensure compliance with ISO 20022 standards and enhanced electronic channel usage.

She reiterated that there was no “KYC zero” policy, emphasizing that all institutions must ensure proper know-your-customer (KYC), know-your-business (KYB), and customer due diligence (CDD) procedures are strictly enforced.

She said: “We have KYC 1, 2 and 3, with different thresholds. There is no KYC called KYC zero, where there is no identity at all.

“The central bank has not come up with a policy on any category called KYC four. So if you have that in your books, it will be very expedient that you address them.”

For users, the directive raises cautious optimism. Chidiebere David Livinus, a resident of Imo State who has experienced multiple failed transfers, said the announcement gives some hope but does not erase years of frustration.

“I have reported cases where my money was stuck for more than one week,” he said.

“If banks can truly start acting within 30 minutes, it will reduce stress. But we need to see refunds happening faster, not just messages saying they are investigating.”

“Looking at industry fraud over the past five years, the number of cases has declined significantly… If we must achieve financial inclusion, fraud must be driven as close to zero as possible. It is achievable,” Oiwoh told reporters during the session.

Between Policy and Practice

Nigeria has introduced several digital finance reforms over the years. The main challenge has rarely been policy design, but consistent implementation. For those at the frontline of digital payments, trust is built not by circulars or press releases, but by outcomes.

“If my money comes back quickly, I will believe,” Ibrahim Usman, a POS operator.

“If it still takes days or weeks, then nothing has changed.”

This report is produced under the DPI Africa Journalism Fellowship Programme of the Media Foundation for West Africa and Co-Develop.